Your 2025 Safety Net Playbook: Where Smart Savers Are Parking Their ‘Untouchable’ Cash After Fed Rate Cuts

Fed rate cuts have quietly flipped the script on where your just-in-case money belongs.

For the last two years, tossing your emergency fund into a high-yield savings account (HYSA) was almost a no-brainer—5%+ APYs with zero risk felt like cheating the system.

In late 2025, those same accounts are still strong, but yields are drifting down, and savers who don’t adjust may leave thousands on the table over the next decade.[1][2][3]

So the real question isn’t “What’s the best savings account?”—it’s: Given today’s lower-rate world, what’s the smartest mix of cash vehicles for your emergency fund?

The 2025 Reality Check: What You’re Earning on ‘Safe’ Cash Right Now

As of December 2025, the top HYSAs still pay meaningfully more than big brick-and-mortar banks, but the peak is clearly behind us.[1][2][3]

Here’s a snapshot of current yields:

- High-yield savings accounts (online, variable rate):

Varo Savings up to 5.00% APY on balances to $5,000 with requirements; Newtek Bank around 4.35% APY; Axos Bank around 4.31% APY.[1][2][3] - Other competitive HYSAs:

Openbank at about 4.20% APY, Marcus by Goldman Sachs around 3.65% APY, Synchrony Bank around 3.65% APY.[3][4][5][6] - Traditional savings at big banks: often around the FDIC national average of roughly 0.40% APY—practically rounding error.[1][2][3]

At the same time, the top-quoted CD rates have slipped—recent lists show many 1-year CDs landing in the mid–3% to low–4% range, down from their 2023–2024 highs.[2][4]

Money market accounts and short-term Treasuries are also resetting lower as the Fed eases policy.

Translation: cash is still being rewarded, but the free 5% lunch is going away.

You now have to be more deliberate about what portion of your safety net stays ultra-liquid in an HYSA and what portion can work a bit harder.

The Four Main Parking Spots for Your Emergency Money in 2025

1. High-Yield Savings: Still the Default ‘First Line of Defense’

HYSAs remain the core for most emergency funds for one simple reason: instant access with FDIC or NCUA insurance up to $250,000 per institution.[1][2][3]

Accounts like Varo, Newtek, Axos, Openbank, Synchrony, and Marcus all fall in this camp.[1][3][4][5][6]

Pros:

- Fast access via transfers; some (e.g., Synchrony) offer ATM access for extra liquidity.[5]

- No early-withdrawal penalties.

- Rates still 8–10x national average.[1][2][3]

Cons:

- Rates are variable—if the Fed cuts further, your APY will likely follow.[1][2]

- Top teaser rates (like 5.00% at Varo) may have balance caps or conditions, limiting how much of a large emergency fund can earn the headline rate.[3]

Who should prioritize HYSAs: anyone who might need money in days, not weeks—gig workers, single-income households, or anyone with volatile income.

2. Money Market Accounts: For People Who Want Checkbook-Level Access

Money market accounts (MMAs) sit between HYSAs and checking accounts.

Many banks now advertise MMAs with yields similar to, or slightly below, their high-yield savings offerings, plus check-writing or debit access.

Pros:

- Check-writing and debit card access—good for real emergencies when you need to pay directly.

- FDIC/NCUA insured when offered by banks/credit unions.

Cons:

- APYs can lag the best online savings rates.

- Some require higher minimum balances to earn top yields.

Best fit: households that value frictionless spending access for emergencies and are willing to trade a bit of yield for that convenience.

3. Short-Term CDs: Locking In Yield Before It Slides Further

With HYSA rates already slipping, short-term CDs (6–18 months) are a way to lock in today’s yield and protect part of your emergency fund from future cuts.[2][4]

Top 1-year CDs from online banks recently clustered in the ~3.5–4.2% APY range, depending on issuer and deposit size.[2][4]

Pros:

- Guaranteed rate for the term—no surprises if HYSA yields drop.

- Still FDIC/NCUA insured up to $250,000 per institution.

Cons:

- Early withdrawal penalty if you tap the money before maturity.

- Not ideal for the first 1–2 months of expenses; better for the “deep backup” layer.

Best fit: stable-income households that can handle most shocks using an HYSA and only rarely need the deeper backup layer.

4. Short-Term Treasuries & T-Bill ETFs: For Those Comfortable With a Bit More Complexity

Short-term U.S. Treasuries—bought directly or via low-cost ETFs—offer government backing and potentially competitive yields versus HYSAs and CDs.

As rates fall, though, the advantage shrinks, and price fluctuations become more noticeable.

Pros:

- Backed by the U.S. government.

- State tax advantages on interest for many investors.

Cons:

- Market price can move, especially if you use ETFs.

- Access is not as instant as transferring from a savings account; you must sell or redeem.

Best fit: higher balances, higher tax brackets, and investors already comfortable with brokerage accounts.

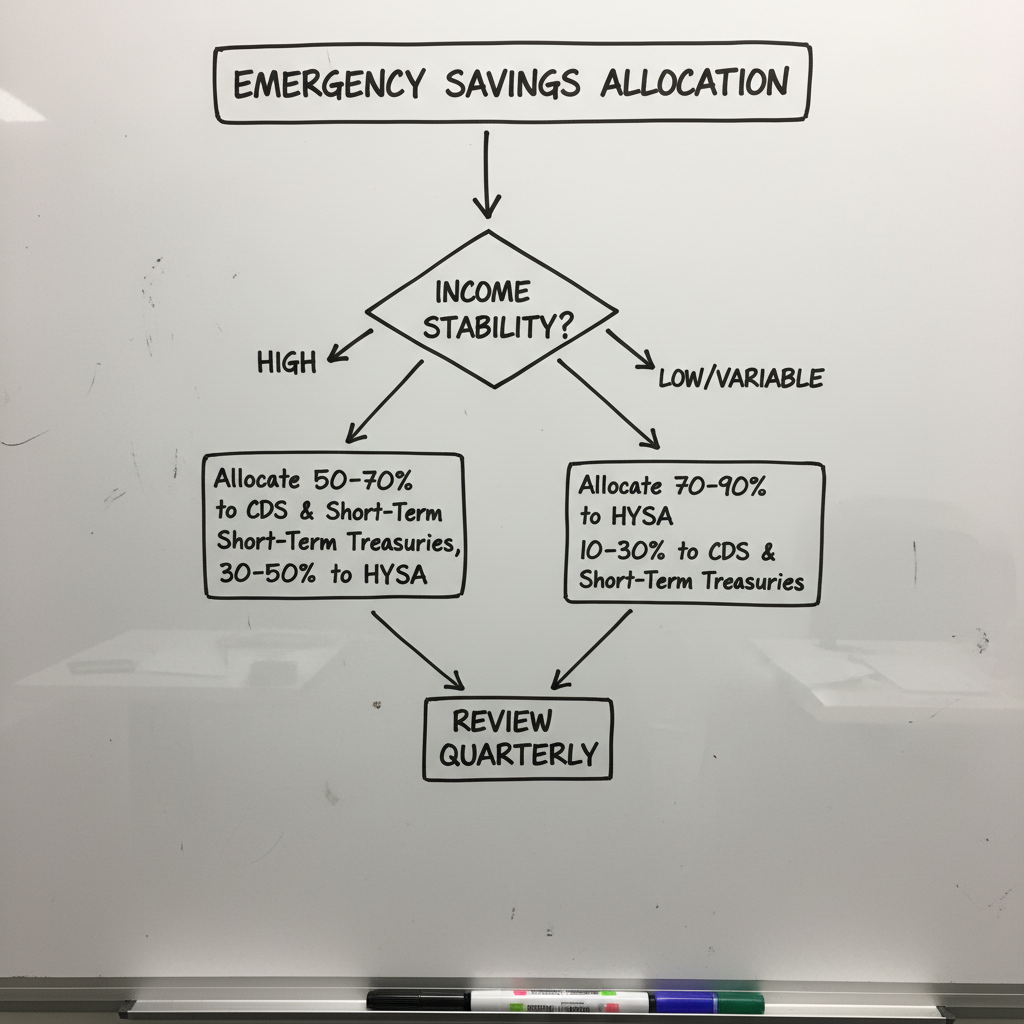

Your 2025 Emergency Fund Decision Tree

Use this simple framework to decide how much to keep in an HYSA vs other options.

Step 1: Rate Your Income Stability

- Unstable income (freelancer, commission-based, startup, single income household):

Aim for 6–12 months of expenses, with at least 3–6 months in an HYSA or MMA at banks like Openbank (4.20% APY), Newtek (4.35% APY), or Axos (4.31% APY).[3][4] - Stable income (W-2, in-demand profession, dual incomes):

3–6 months is often reasonable, with perhaps only 1–2 months fully ultra-liquid and the rest laddered into CDs or Treasuries.

Step 2: Decide How Fast You Might Need to Spend

- “I might need thousands tomorrow.”

Put that amount in a no-penalty, easy-transfer HYSA such as Marcus (around 3.65% APY), SoFi (around 3.60% APY), or Synchrony (around 3.65% APY with ATM access).[3][5] - “I’d have at least a week or two of warning.”

Consider moving the second layer (e.g., months 2–4 of expenses) into a 6–12 month CD from a bank like Openbank or Peak Bank, which have been posting ~4.20% APY on some products.[4][6]

Step 3: Choose Your Mix Based on Risk Tolerance

Here are three model setups you can copy-paste and tweak.

1) The Ultra-Cautious Setup (Maximum Sleep-at-Night Factor)

- 100% of emergency fund in one or two top HYSAs (e.g., Varo up to 5.00% on the first $5,000, then Newtek or Axos for the rest).[1][2][3]

- Optional: split across two different banks to double FDIC coverage and reduce tech/outage risk.

This is the pure “liquidity over yield” play, but in 2025 you’re still earning 4–5% on much of that cash if you pick well.[1][2][3]

2) The Rate-Lock Setup (Protect Against Future Cuts)

- First 2–3 months of expenses in an HYSA (Openbank, Synchrony, Marcus, SoFi).[3][4][5]

- Next 3–9 months laddered into 6–18 month CDs at ~3.75–4.20% APY from online banks.[2][4]

This setup builds in FOMO protection: even if HYSA rates slide another 0.5–1.0 percentage point, a chunk of your cash keeps its higher locked-in yield.

3) The Tax-Savvy Setup (For Larger, More Sophisticated Portfolios)

- 1–2 months in an HYSA for instant access.

- 2–4 months in short-term CDs.

- Remainder in a short-term Treasury or T-bill ETF in a brokerage account.

This is where slightly more advanced savers squeeze extra basis points from tax benefits and Treasury-backed safety, while still keeping everything in the “very low risk” bucket.

Concrete Next Moves You Can Take This Week

If your emergency fund is still languishing at 0.40% in a big-bank savings account, the opportunity cost is no longer theoretical.[1][2][3]

On $20,000, the difference between 0.40% and 4.20% is roughly $760 in one year—money future-you will definitely wish you had.

Here’s a 5-step checklist you can follow immediately:

- 1. Audit your current yield.

Log into your bank, find the APY on your savings, and write it down. - 2. Set a target mix.

Decide: do you want the Ultra-Cautious, Rate-Lock, or Tax-Savvy setup? - 3. Open 1–2 new accounts.

For instant liquidity, consider:

– Varo Savings (up to 5.00% on first $5,000 with requirements)[1][3]

– Newtek (around 4.35% APY)[1][2][3]

– Axos (around 4.31% APY)[1][2][3]

– Openbank or Peak Bank (around 4.20% APY)[4][6] - 4. Move in layers, not all at once.

First transfer one month of expenses to your new HYSA.

Once it clears and you’ve tested access, move the remaining target amount. - 5. Calendar a 6-month review.

Because rates move with the Fed, set a reminder to re-check your APYs and CD maturities twice a year.[1][2]

Why Savvy Savers Are Acting Before the Next Cut

There is a genuine urgency in 2025: once the Fed finishes this rate-cut cycle, today’s 4–5% yields on safe cash could look like a historic blip—just as 2020’s sub-1% felt unthinkable after 2023.[1][2]

Those who move now can lock in part of the current environment and design a safety net that’s both resilient and reasonably rewarding.

Your emergency fund is not about chasing every last basis point.

It’s about making sure a layoff, medical bill, or surprise move doesn’t derail your entire financial plan.

But in a world where smart savers are quietly earning hundreds more per year on the same pile of cash, staying in a 0.40% account is no longer “cautious”—it’s just expensive.

Action step: before you close this tab, pick one thing: either open a modern HYSA, set up a small CD ladder, or schedule that 6-month review.

Future-you will thank you the next time life throws a curveball—and your 2025 safety net will be ready.

Unlock Full Article

Watch a quick video to get instant access.