Buying a home is one of the biggest financial decisions you’ll ever make—and getting the best mortgage rate can save you thousands over the life of the loan. Yet, many homebuyers rush through the process or accept the first offer they get. Whether you’re a first-time buyer or looking to refinance, here are five simple but essential steps to help you shop smart and land the best mortgage rate possible.

1. Check and Improve Your Credit Score

Your credit score plays a huge role in determining the interest rate lenders offer you. The higher your score, the better your rate. Before applying, get a copy of your credit report from all three major bureaus (Experian, TransUnion, and Equifax). Dispute any errors you find and work on paying down existing debts. Even a small increase in your score can lead to big savings over the life of your mortgage.

Tip: Aim for a credit score of at least 740 to qualify for the most competitive rates.

2. Know Your Budget and Get Pre-Approved

Before you fall in love with a home, know how much house you can afford. Use mortgage calculators to estimate your monthly payments, taking into account taxes, insurance, and potential HOA fees. Once you have a clear picture, get pre-approved by a lender. This not only strengthens your offer when bidding on a home but also gives you a concrete idea of the rates and loan amount you qualify for.

Remember, pre-qualification is not the same as pre-approval. Pre-approval requires a more detailed review of your finances and holds more weight with sellers.

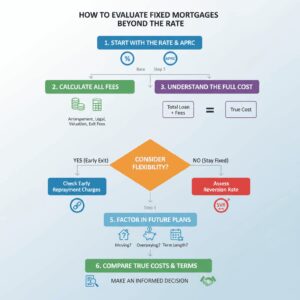

3. Shop Around and Compare Lenders

Don’t make the mistake of settling for the first quote you get. Rates and fees can vary widely between lenders, so it’s crucial to shop around. Get estimates from at least three to five lenders—including banks, credit unions, and online mortgage companies. When comparing, look beyond just the interest rate. Pay attention to APR (which includes fees), loan terms, and any special conditions.

Tip: All mortgage inquiries made within a 45-day window are typically treated as one inquiry on your credit report, so it won’t significantly hurt your score.

4. Understand Points and Fees

Lenders may offer the option to pay discount points—upfront fees that lower your interest rate. This can be worth it if you plan to stay in the home long-term, but it’s not always the best option. Compare the cost of points versus the monthly savings they bring. Also, watch out for other fees such as loan origination, underwriting, and application fees. Ask for a Loan Estimate form from each lender, which breaks down all the costs so you can compare them apples-to-apples.

5. Lock In Your Rate at the Right Time

Mortgage rates can change daily based on market conditions. Once you find a rate you’re happy with, ask your lender to lock it in. This guarantees your rate for a set period—usually 30 to 60 days—protecting you from increases while you finalize your home purchase.

If rates are falling or you’re not in a rush, you might hold off on locking in. But if rates are trending upward or your closing is near, a rate lock can provide peace of mind.

Shopping for a mortgage doesn’t have to be overwhelming. By understanding your credit, setting a realistic budget, comparing lenders, reviewing the fine print, and timing your rate lock strategically, you can take control of the process and secure the best deal possible. With a little prep and patience, you’ll be one step closer to moving into your dream home—without overpaying on your mortgage.