Refinancing your mortgage makes sense when it lowers your interest rate or reduces your monthly payments. It can also be beneficial to shorten the loan term.

Refinancing a mortgage involves replacing your current loan with a new one, often with better terms. Homeowners refinance to save money, access home equity, or switch from an adjustable-rate to a fixed-rate mortgage. Before deciding, consider the costs involved, such as closing fees and appraisal charges.

Calculate your break-even point to determine when you’ll recoup these costs. It’s essential to have a good credit score to secure favorable rates. Refinancing can significantly impact your financial health, so evaluate your goals and consult a financial advisor. Make sure the benefits outweigh the costs to make an informed decision.

Introduction To Mortgage Refinancing

Mortgage refinancing means getting a new loan to replace the old one. The new loan often has better terms. This can include a lower interest rate or monthly payment. Many people refinance to save money.

Refinancing can also help you pay off your mortgage faster. Others might want to switch from an adjustable-rate mortgage to a fixed-rate mortgage. This can provide more stability in payments.

There are several common reasons people choose to refinance their mortgage:

- Lowering the interest rate

- Reducing the monthly payment

- Changing the loan term

- Switching from an adjustable-rate to a fixed-rate mortgage

- Accessing home equity for cash

When To Consider Refinancing

Interest rates can drop significantly. This can be a great time to refinance. Lower rates can save you money. Monthly payments can become more manageable. You may pay less over the life of your loan. Always compare rates from different lenders. This will help you find the best deal.

A better credit score can open doors. You might qualify for better loan terms. This means lower interest rates. Your monthly payments can decrease. You can save thousands over time. Check your credit score regularly. Aim to improve it before refinancing.

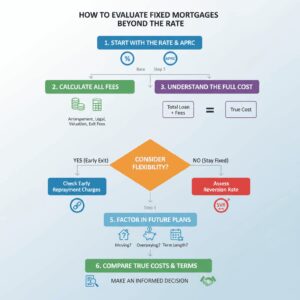

Calculating The Break-even Point

The break-even point is very important. It shows how long to recover the refinancing costs. To find this, you need to know some numbers. First, find the total refinancing costs. Next, calculate the monthly savings from the new loan.

To calculate the break-even point, use this formula: Divide the total refinancing costs by the monthly savings. The result is the number of months to break even. For example, if refinancing costs $3,000 and monthly savings are $150, it takes 20 months to break even.

Types Of Mortgage Refinancing

Rate-and-term refinance changes the interest rate or loan term. This option is good for lowering monthly payments. It can also help in paying off the loan faster. Sometimes, it reduces the total interest paid over the loan’s life. Homeowners often choose this to take advantage of lower interest rates.

Cash-out refinance replaces your old loan with a new one. The new loan is larger than the existing mortgage. The difference is paid out in cash. Homeowners use this extra money for home improvements or debt consolidation. It can also be used for other financial needs.

Costs Involved In Refinancing

Closing costs include various fees. These fees add up quickly. Lenders charge origination fees. Title insurance is also needed. Recording fees are required. These fees can total thousands of dollars. It’s important to budget for them.

Appraisal fees are necessary. The lender needs to know your home’s value. This ensures the loan is secured. Appraisal fees range from $300 to $500. The cost depends on your location. It’s a one-time fee. Pay this fee at the start of the process.

Benefits Of Refinancing

Refinancing your mortgage can lead to lower monthly payments. This means you will have more money each month. These extra funds can be used for other needs or savings. It can make your life easier financially. Lower payments can help you manage your budget better.

Refinancing can also give you a shorter loan term. This means you can pay off your mortgage faster. A shorter term can save you money on interest. Paying off your loan quickly can give you financial freedom sooner. It can also increase your home equity faster.

Potential Risks And Drawbacks

Some loans have prepayment penalties. These are fees for paying off a loan early. These fees can be quite high. It makes refinancing more expensive. Always check for these penalties in your current loan agreement. Talking to your lender can help you understand these fees better.

Refinancing can sometimes extend your break-even period. The break-even period is when you start saving money. It means you might pay more in the long run. Even if monthly payments are lower, the total cost can be higher. Make sure to calculate this period before refinancing.

Steps To Refinance Your Mortgage

Collecting financial documents is a must. Start with your tax returns and pay stubs. Include bank statements and investment accounts. Organize loan documents and credit card statements. Ensure everything is up-to-date. This will help in the approval process.

Compare different lenders for the best rates. Look at interest rates and fees. Check customer reviews and ratings. Ask for quotes and pre-approvals. Choose a lender with the best terms. This can save you money over time.

Conclusion

Refinancing your mortgage can offer significant benefits. Evaluate your financial situation and goals carefully. Lower interest rates or better terms might save you money. Always consider closing costs and long-term implications. Consult with a financial advisor to make the best decision for your needs.

Refinancing could be a smart move for your future.

Unlock Full Article

Watch a quick video to get instant access.