Late Starter’s Playbook: Best Long-Term Care Insurance Moves for Retirees Buying Coverage After 65

Late Starter’s Playbook: Best Long-Term Care Insurance Moves for Retirees Buying Coverage After 65

You’re 67, retired, and suddenly facing the reality that long-term care isn’t just a distant concern—it’s a financial threat that could drain your retirement savings in months. The good news? You’re not alone, and contrary to what you might think, it’s not too late. The 2026 long-term care insurance market has evolved to serve late starters like you with realistic options that don’t require a medical degree to understand or a second mortgage to afford.

This guide cuts through the noise and gives you the concrete next steps to protect your retirement without overpaying or getting trapped in underwriting limbo.

Why Age 65+ Changes Everything (And Why It’s Still Manageable)

Traditional long-term care insurance becomes significantly more expensive after 65. Premiums spike, underwriting tightens, and insurers scrutinize pre-existing conditions more closely. But here’s the plot twist: the market has adapted. Insurers now recognize that retirees buying coverage after 65 represent a growing segment, and they’ve created products specifically designed for this demographic.

The key difference? You’re no longer shopping for coverage that might never be used. You’re buying protection for a risk that’s statistically more likely to materialize within your lifetime. That fundamental shift has opened doors to shorter-term policies, hybrid products, and simplified underwriting processes that didn’t exist five years ago.

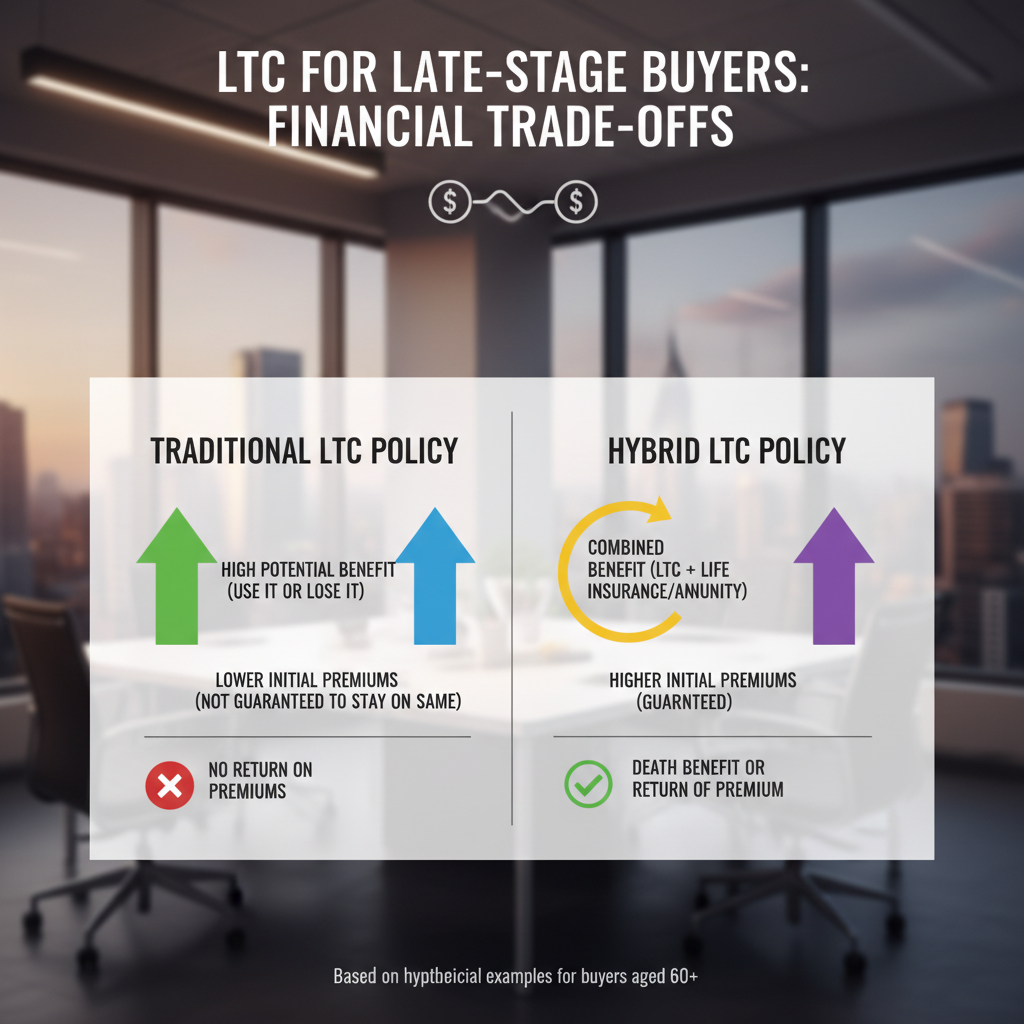

Option 1: Traditional Long-Term Care Insurance (If You’re Healthy)

Mutual of Omaha: Best for Late-Issue Ages

Mutual of Omaha currently leads the market for retirees purchasing coverage after 65, offering policies to ages 79 with competitive pricing and strong claims performance. Their MutualCare Secure Solution and MutualCare Custom Solution both feature built-in cash benefits with no elimination periods—meaning you get paid immediately when you need care, not after waiting 90 days.

What makes Mutual of Omaha stand out for your age group: monthly benefits range from $1,500 to $10,000, with benefit periods of 2-5 years. For a 67-year-old in good health, you’re looking at realistic premiums that don’t require cutting your golf budget. The policies cover nursing home care, assisted living, home health care, respite care, and hospice services. International coverage is included—full benefits in the U.S., U.K., and Canada, plus up to one year anywhere else.

Recent enhancement: Mutual of Omaha has increased maximum monthly benefits to $15,000 per month (before inflation protection), crucial for retirees in high-cost-of-living areas like California or New York.

National Guardian Life: Flexible for Late Starters

National Guardian Life (NGL) offers customizable features including Lifetime Benefits, Return of Premium riders, and flexible premium payment options. For couples, they offer shared care options—if one spouse exhausts their coverage, the other can tap into remaining benefits. This is a game-changer if you’re married and worried about one partner’s care consuming all available benefits.

Option 2: Hybrid Life/LTC Policies (The Smart Play for 2026)

Here’s where the market has truly shifted in your favor. Hybrid policies combine life insurance with long-term care benefits in a single contract. If you never need long-term care, your beneficiaries receive the death benefit. If you do need care, you can access those funds tax-free for eligible expenses. It’s insurance that pays you either way.

Why Hybrids Win in 2026

Higher interest rates have made hybrid policies significantly more attractive than they were in 2024-2025. The enhanced returns mean better cash value accumulation and stronger long-term care benefits for the same premium. This is temporary—when rates eventually decline, these products will become less attractive, creating urgency for 2026 buyers.

Lincoln Financial MoneyGuard: Market Leader

Lincoln Financial’s MoneyGuard is the dominant hybrid product for retirees. It combines life insurance with long-term care benefits, strong cash value accumulation, and multiple payment schedules. Lincoln Financial’s A+ rating from AM Best and Fitch gives policyholders confidence in claims performance.

For late starters: You can fund MoneyGuard with a single premium (or flexible payments), making it simpler than traditional policies. If you have $50,000-$100,000 sitting in a low-yield savings account, a single-premium MoneyGuard could convert that into lifetime care protection plus a death benefit.

Nationwide Care Matters Together: Couples’ Coverage

Nationwide’s Care Matters Together is specifically designed for couples and features lifetime/unlimited LTC benefits with cash benefit options. The policy covers both spouses with a shared pool of benefits, competitive pricing, and flexible underwriting. The simplified underwriting process—no phone interview required—is crucial for retirees with pre-existing conditions or complex medical histories.

Nationwide also accepts IRA/401(k) rollovers for premium funding. This is significant: you can fund your long-term care insurance with pre-tax retirement dollars, potentially reducing your taxable income while protecting your assets.

Option 3: Short-Term Care & Backup Plans

When Traditional Underwriting Fails

If you’ve been declined for traditional long-term care insurance or hybrid policies due to pre-existing conditions, Nationwide Financial offers lenient underwriting on their annuity products with long-term care riders. This isn’t ideal, but it’s better than zero protection.

Short-term care policies (2-3 year benefit periods) are also more underwriting-friendly for retirees with health issues. While they won’t cover a decade-long care scenario, they bridge the gap during the most expensive early years of care, buying time for family support or other resources to kick in.

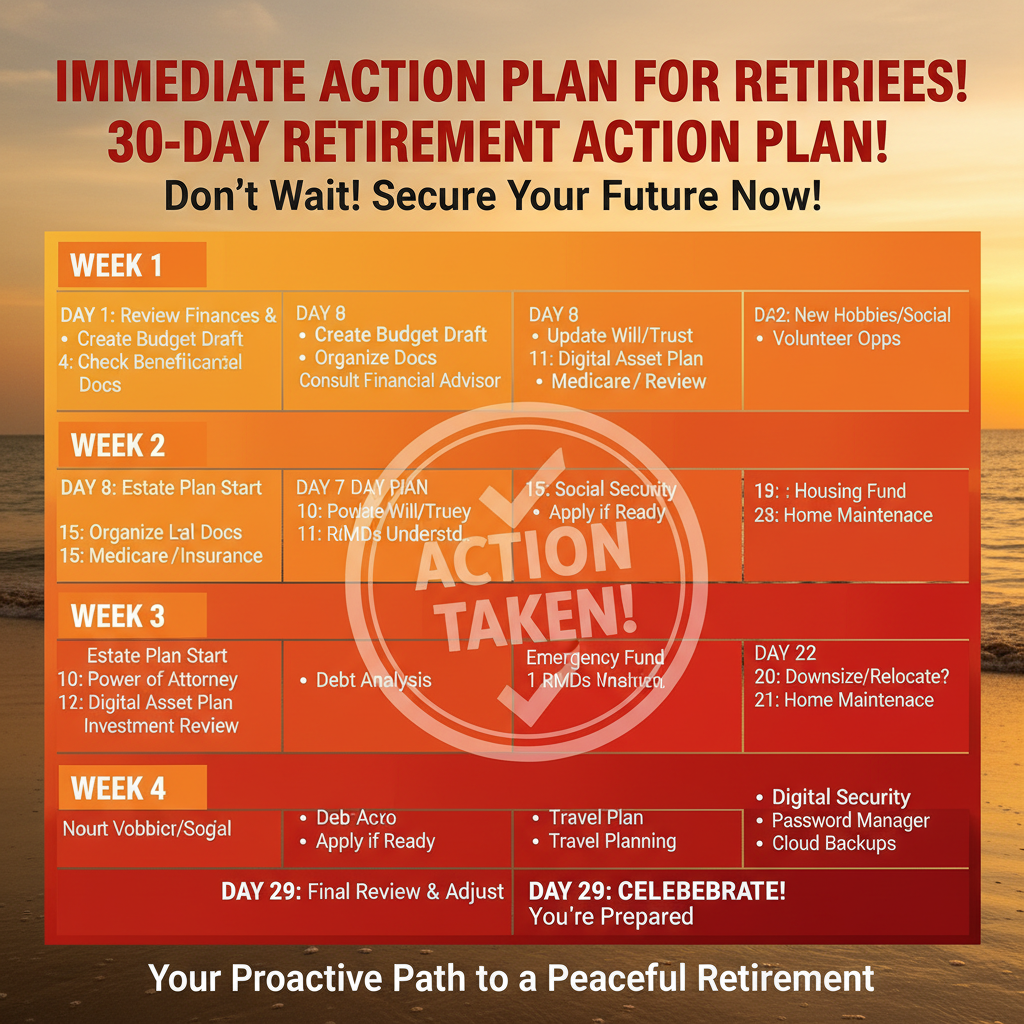

Actionable Steps: Your 30-Day Action Plan

Week 1: Assess Your Situation

- Get your current health status documented (blood pressure, cholesterol, medications, recent diagnoses)

- Calculate your potential long-term care costs in your area (nursing home: $8,000-$15,000/month; assisted living: $4,500-$8,000/month)

- Determine how many years of care you could self-fund before retirement savings are depleted

Week 2: Get Quotes from Three Carriers

- Request quotes from Mutual of Omaha, Nationwide, and Lincoln Financial

- For each, ask about: maximum monthly benefits, elimination periods, inflation riders, and return of premium options

- Compare apples-to-apples (same benefit amount, same benefit period)

Week 3-4: Work with an Agent

- Find an independent agent who represents multiple carriers (not captive to one company)

- Have them explain underwriting requirements and timeline

- If declined, ask about simplified underwriting or short-term alternatives

Critical Pricing Reality for 2026

For a healthy 67-year-old couple purchasing a traditional policy with $3,000/month benefit and 5-year benefit period, expect to pay $150-$250/month combined. A hybrid single-premium policy funded with $75,000 might provide $3,000/month care benefit plus a $100,000+ death benefit.

These aren’t small numbers, but they’re significantly smaller than the $100,000-$300,000 cost of a single year in a nursing home. The math is brutal: one year of care costs what you’d pay in premiums over 20-30 years.

The Urgency Factor: Why 2026 Matters

Interest rates are elevated, making hybrid products exceptionally valuable right now. Underwriting is becoming stricter as carriers tighten risk pools. Your health is unlikely to improve. Premiums will only increase as you age. Every year you wait costs you thousands in additional premiums.

This isn’t fear-mongering—it’s math. A policy purchased at 67 versus 70 saves you 36 months of premiums, and the earlier purchase price locks in a lower rate for life.

Final Thoughts: You’re Not Too Late

The narrative that long-term care insurance is only for 55-year-olds is outdated. The 2026 market has evolved to serve retirees who are finally confronting this reality. You have real options, realistic pricing, and a clear path forward. The only mistake is inaction.

Start this week. Get quotes. Have conversations. The peace of mind—knowing your retirement savings won’t be decimated by care costs—is worth the effort.

Unlock Full Article

Watch a quick video to get instant access.