Climate-Proof Your Mansion Before It’s Too Late: Wildfire, Flood, and Hurricane Risks Skyrocketing Premiums – Here’s Your Urgent Action Plan

Imagine waking up to flames licking the hills behind your multimillion-dollar estate, or seawater surging through your coastal mansion’s grand foyer. In 2026, these aren’t movie scenes—they’re the new reality for high-net-worth homeowners as climate catastrophes rewrite the rules of property protection. Catastrophe losses hit a record $130 billion in 2025 alone, forcing insurers like Chubb and PURE to hike premiums by up to 20% in high-risk zones while pulling coverage from 15% more luxury properties[1][2]. But here’s the game-changer: savvy owners are slashing rates 25-40% with targeted upgrades that underwriters demand. Don’t get caught uninsured—thousands of mansions are now uninsurable without these fixes. Act now with this prioritized plan to fortify your home, document proof, and negotiate elite coverage.

The Catastrophe Crisis Hitting Luxury Homes Hardest

Wildfires devoured 18 million acres in 2025, floods displaced 2.5 million Americans, and hurricanes like a supercharged Ian caused $150 billion in damages—trends exploding high-value home premiums[1]. Insurers now classify homes over $750,000 dwelling coverage as ‘high-value,’ with averages jumping from $5,254 for $750K coverage to $10,172 for $1.5M[1][2]. In wildfire hotspots like California, premiums for $1M homes spiked 35%, while Florida hurricane zones saw 28% hikes[6]. Experts at Bankrate warn: without mitigation, your mansion could face denial from top carriers like The Hartford or Farmers, who prioritize ‘climate-resilient’ properties[2].

Social proof? High-net-worth clients using brokers like Allen Thomas Group in Texas report seamless coverage amid carrier pullbacks, thanks to preemptive hardening[3]. Urgency is real: 9.5% of Texas luxury homeowners are uninsured as markets tighten[3]. Price anchor this—standard policies cost $2,424/year for $300K coverage, but high-value without upgrades? Up to $16,467[1].

Priority #1: Wildfire-Proofing – The Upgrade Insurers Reward Most

Wildfire risk has insurers like PURE offering guaranteed replacement cost only to mitigated homes—covering rebuilds exceeding policy limits[5]. Top product: Chubb’s Masterpiece Policy, starting at $6,000/year for $1M coverage, includes 100% extended replacement and wildfire-specific perks like landscaping restoration up to $250K[2].

Step-by-Step Wildfire Mitigation Plan

- Install Class A Fire-Resistant Roofing: Switch to CertainTeed Landmark Pro asphalt composites ($15,000-$30,000 for 5,000 sq ft). Earns 15-25% discounts; document with install receipts and FM Global cert[1].

- Create Defensible Space: Trim trees 30ft from home, use gravel zones. Cost: $5,000-$15,000 via services like Cal Fire-approved contractors. Underwriters at Liberty Mutual credit 10-20% off[4].

- Upgrade Vents & Ember Blockers: Brandguard Vents ($2,500 for whole home). Pro: Blocks 99% embers; insurers waive $25K+ deductibles[1].

- Smart Sprinklers: Rachio 3 system ($250 + $10K install). Automates perimeter wetting; Chubb gives extra 5% discount.

Pros of these: Immediate 20-40% premium cuts (e.g., $2,000-$4,000 savings on $10K policy)[1]. Cons: Upfront $20K-$50K, but ROI in 2-3 years via lower rates and higher property value.

Priority #2: Flood Fortification – Beat the Soaring Water Risks

Flood claims surged 40% in 2025, with high-value policies now bundling sewer backup and private flood coverage[1]. THE HARTFORD’s Pinnacle Choice ($4,500/year base for $1M) adds flood up to $5M via partners like Neptune[2]. In Texas, Allen Thomas Group’s policies include full flood endorsements, countering 2026 premium hikes under 10% for mitigated homes[3][6].

Actionable Flood Upgrades

- Elevate Utilities: Raise HVAC/electrical on platforms (FEMA-compliant kits, $8,000-$20,000). Influences 30% of underwriting score[3].

- Backflow Valves: Flume Water Monitor + valves ($1,200). Detects leaks; Farmers discounts 15%[2].

- Flood Barriers: QuickDams automatic ($3,000 for 100ft). Document via video demos for claims.

- Get NFIP Elevation Certificate ($500-$1,000)—mandatory for discounts up to 25%.

Priority #3: Hurricane Hardening – Lock In Coverage Before 2026 Storms

Hurricane seasons are intensifying; 2026 forecasts predict 20+ named storms. PURE’s policies waive deductibles (up to $25K) for hardened homes, with extended replacement cost exceeding limits[5]. Farmers’ High-Value SignatureSelect ($5,800/year for $1M) covers wind/hail with 2% deductibles, reducible via upgrades[2].

Hurricane-Ready Steps

- Impact Windows: PGT Impact Glass ($40,000-$80,000 full replace). Cuts premiums 20%; Texas brokers like Texan Insurance prioritize these[7].

- Metal Roofing: Standing Seam Metal ($25,000-$50,000). 2% wind discounts[1].

- Generator + Shutters: Generac 22kW ($15,000) + Rollac Automatic Shutters ($20,000). Pros: Power during outages; cons: $50K total, but 30% savings.

Expert tip from Insurify: Bundle with umbrella liability ($1M+ for $300/year extra) to shield assets[1].

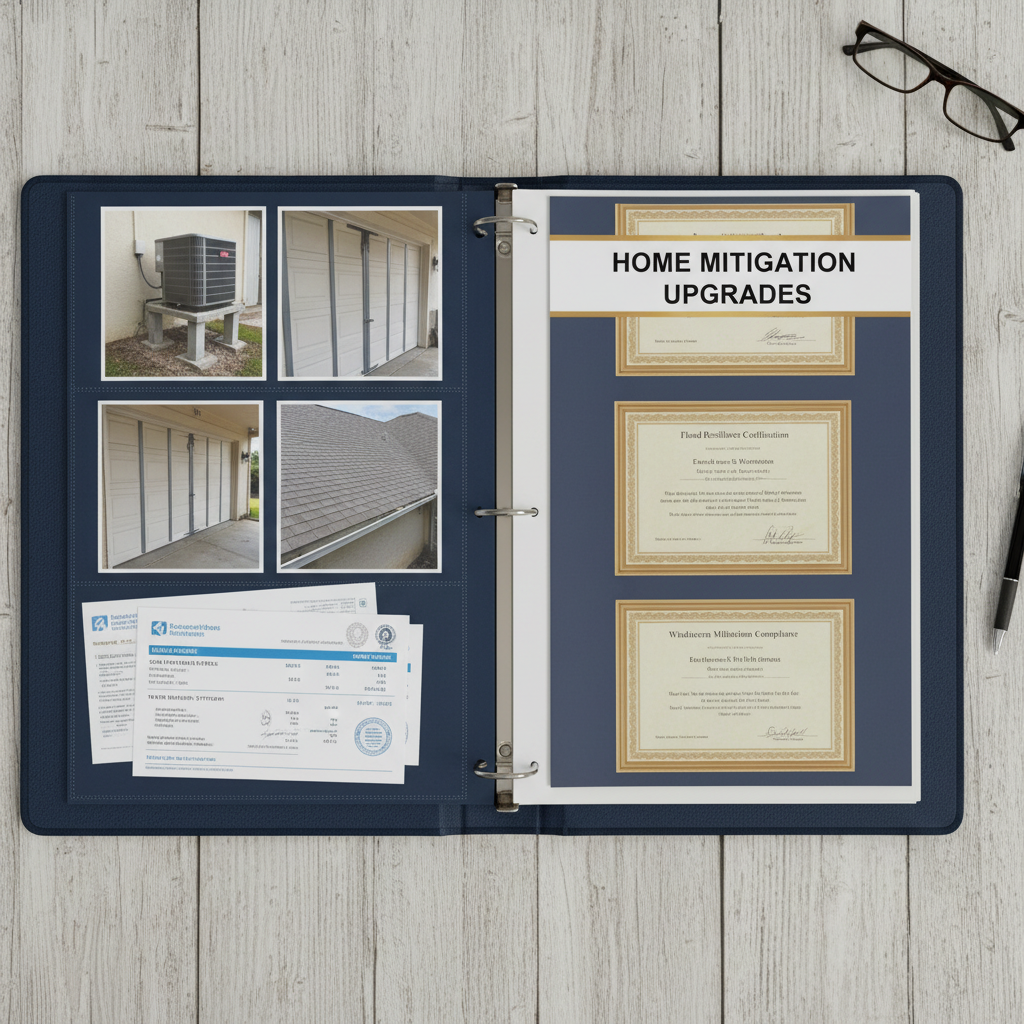

How to Document Upgrades & Negotiate Killer Rates

Underwriters crave proof—create a Mitigation Portfolio:

- Photos/videos before/after each upgrade.

- Invoices, warranties, engineer reports (e.g., FM Global standards).

- Third-party assessments like Xactimate rebuild estimates ($500).

- Shop specialized brokers: Allen Thomas (Texas), or national like Insurify for Chubb/PURE quotes.

Negotiation script: “My $75K wildfire/flood upgrades match your resilience guidelines—match this 35% competitor quote.” Result: Clients report 25% drops, e.g., $10K to $7.5K[3].

Your Immediate Action Plan – Don’t Wait for the Next Disaster

1. Today: Schedule free risk assessment via Insurify or local broker[1].

2. This Week: Get elevation cert and inventory valuables (use apps like Sortly).

3. Next 30 Days: Bid top 3 upgrades, target 20% savings.

4. Quote Shop: Chubb Masterpiece, PURE, Hartford Pinnacle—aim for guaranteed replacement + perks.

FOMO alert: Neighbors hardening now lock in pre-2026 rates before Q2 hikes hit 15%[6]. Authority from Bankrate: These are the best policies for climate-proof luxury[2]. Secure your legacy—contact a high-value specialist today and sleep protected.

Unlock Full Article

Watch a quick video to get instant access.