High-Need Families Deserve Better: How to Find Low-Deductible Health Plans That Actually Cover What Matters in 2026

High-Need Families Deserve Better: How to Find Low-Deductible Health Plans That Actually Cover What Matters in 2026

If your family includes children with asthma, a spouse managing diabetes, or anyone requiring regular therapy or specialist visits, you already know the truth: the cheapest health insurance plan isn’t always the best deal. When you’re facing $5,000+ deductibles on a Bronze plan, that rock-bottom $300/month premium evaporates the moment your kid needs urgent care or your prescription refills kick in.

The real crisis facing high-use families isn’t finding affordable coverage—it’s finding affordable coverage that doesn’t leave you financially devastated when you actually need it. This is where understanding 2026 marketplace dynamics becomes critical. With deductibles rising and monthly premiums climbing faster than ever, families with chronic conditions face an impossible math problem. But there’s a smarter way to shop.

The 2026 Premium Shock: What’s Actually Happening to Family Costs

Let’s start with the hard numbers. For families earning $40,000 annually, health insurance costs after subsidies jumped from $154/month in 2025 to $287/month in 2026—an 86% increase. For those earning $30,000, the jump was even more brutal: from $49 to $155 monthly, a 216% spike. This isn’t theoretical—this is happening right now to millions of American families.

But here’s what matters most for high-need families: these premium increases mask a deeper problem. While you’re shopping for the lowest monthly payment, deductibles and out-of-pocket maximums are the real financial trap. A family of four paying $2,329/month (the current average) could face an additional $9,800 in out-of-pocket costs before insurance truly kicks in.

For families with children requiring ongoing care—therapy sessions, specialist appointments, chronic disease management—this deductible structure is financially devastating. You need a different strategy entirely.

Silver Plans with Cost-Sharing Reductions: The Hidden Gem Most Families Miss

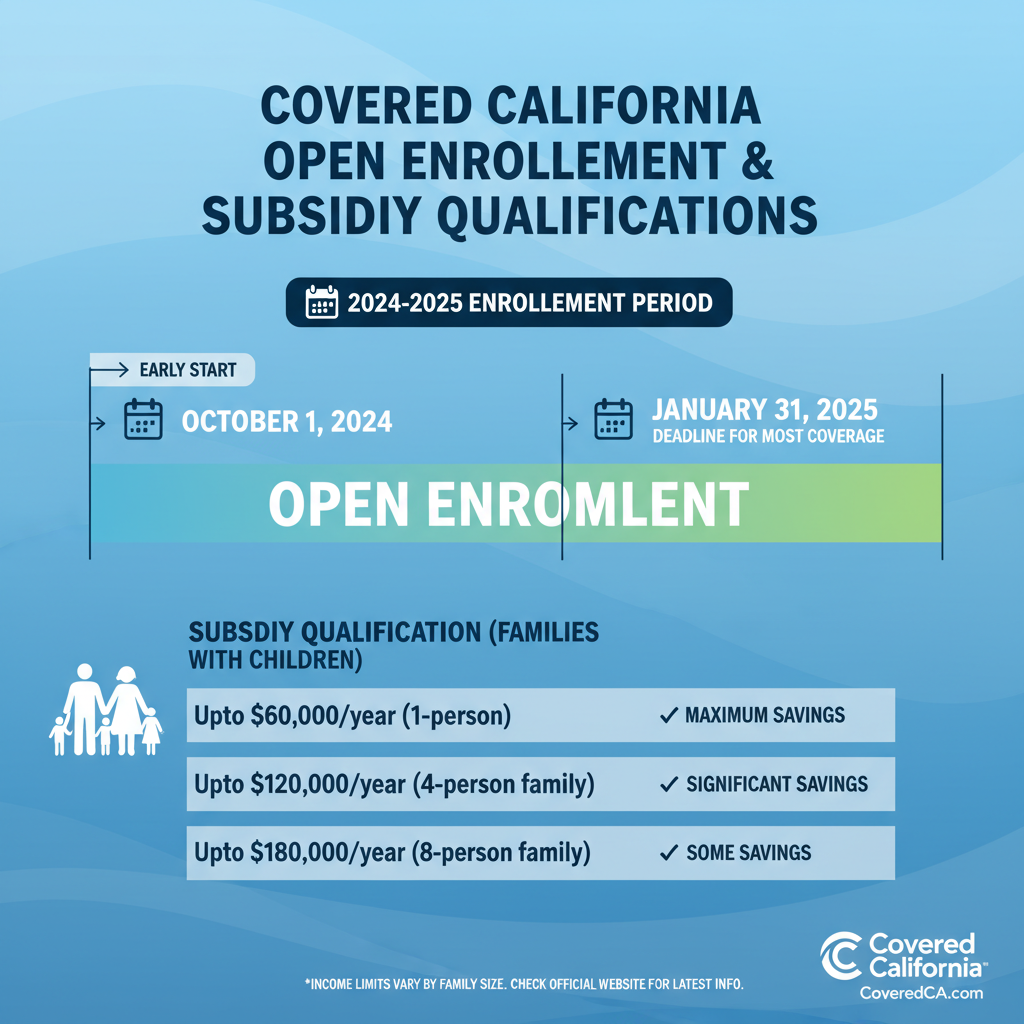

Here’s the secret that changes everything: if your household income falls between $15,650 and $62,600 (for an individual), you likely qualify for federal subsidies that make Silver plans dramatically cheaper than advertised. But there’s a second layer most families don’t know about.

Silver plans offer something called Cost-Sharing Reductions (CSR) if you earn up to approximately $39,000 (individual) or $80,000 (family of four). When you qualify, these plans automatically reduce your deductible, copays, and coinsurance—sometimes to nearly zero. On Covered California, look for plans marked “Silver CSR” in green with “extra savings” labels.

The real kicker: families who qualify for CSR often get comprehensive coverage for less than $25/month. Not $250. Not $125. Less than $25. This isn’t a loss-leader or promotional rate—it’s the actual 2026 marketplace structure for qualified families.

For a family with a child requiring monthly therapy, regular pediatrician visits, and asthma management, this difference is the gap between financial stability and medical debt.

Comparing the Actual Players: Who Delivers Low Deductibles + Affordability

Not all affordable insurers are created equal when you have high healthcare needs. Let’s look at real 2026 pricing for Silver 70 HMO plans (the sweet spot for families):

L.A. Care Health Plan: $402/month for a 40-year-old. This is the lowest-cost option across California, with an average deductible of $5,200 and out-of-pocket maximum of $9,800. Availability is limited (primarily Southern California), but if you’re in their service area, this is your baseline benchmark.

Molina Healthcare: $491/month with identical deductible and out-of-pocket structure. Molina has broader geographic coverage than L.A. Care and consistently ranks among the most affordable options statewide.

Kaiser Permanente: $592/month for their Silver 70 HMO. Higher premium, but Kaiser’s integrated delivery model means lower specialist referral friction and better coordination for families managing multiple conditions. For families with kids in therapy or requiring specialist care, the coordination benefits often justify the $90-190 monthly premium difference.

Health Net: $525/month through their Ambetter offering. Strong middle ground with reasonable deductibles and broader network access than HMO-only plans.

The critical insight: switching from the most expensive to cheapest Silver plan in California saves $706/month. But for high-need families, that’s not the real metric. The real metric is total out-of-pocket cost including deductibles, copays, and specialist visit costs.

The Drug Formulary and Specialist Visit Analysis: Where Cheap Plans Get Expensive

Here’s where most families make costly mistakes: they compare premiums without analyzing drug formularies or specialist coverage. A plan saving you $100/month becomes worthless if your child’s ADHD medication isn’t covered or requires prior authorization delays.

For 2026, before you commit to any plan:

Step 1: List Every Current Medication – Check each insurer’s formulary (available on their website) for your family’s exact prescriptions. Don’t assume generic alternatives work—some families have discovered their child’s medication isn’t covered until after enrollment.

Step 2: Verify Specialist Access – Call the insurer directly. Ask: “How many pediatric therapists are in-network?” “What’s the typical wait time for a new patient appointment with a pediatric endocrinologist?” Plans with lower premiums sometimes have minimal specialist networks.

Step 3: Calculate Total Expected Costs – Don’t just add premium + deductible. Factor in copays for monthly therapy ($30-50 per visit × 4 visits/month = $120-200), specialist visits ($40-100 each), and prescription costs. A family spending $500/month on therapy copays needs a plan with lower copays, even if the premium is higher.

Step 4: Compare Out-of-Pocket Maximums – This is your financial ceiling. Most Silver plans cap out around $9,800 per individual or $19,600 per family. Platinum plans (highest tier) sometimes reduce this to $6,000-7,000. For high-use families, the Platinum premium difference might be $200-300/month, but it caps your maximum exposure lower—often a worthwhile trade.

Medi-Cal: The Option Nobody Talks About (But Should)

If your household income is below approximately $22,000 (individual) or $44,000 (family of four), you likely qualify for Medi-Cal, California’s Medicaid program. Medi-Cal covers you at zero cost. No premiums. No deductibles. No out-of-pocket costs.

For families with children, this is even more generous: children may qualify for free Medi-Cal coverage even if parents don’t. This means your kids get comprehensive coverage including dental, vision, and therapy—all free—while you navigate marketplace plans.

Don’t overlook Medi-Cal because you think you “don’t qualify.” Enrollment is available year-round (unlike marketplace plans), and the application process through Covered California takes minutes.

The 2026 Shopping Strategy: Your Action Plan

Timeline: Open Enrollment runs November 1 through January 15 each year. Outside this window, you need a qualifying life event (birth, job loss, marriage) to enroll.

Tool: Use Covered California’s subsidy calculator (coveredca.com) to see your exact costs in seconds. This shows real 2026 pricing, not estimates.

Comparison: Don’t just compare premiums. Use the plan comparison tool to see deductibles, copays for your specific medications, and specialist visit costs side-by-side.

Enrollment: Choose to apply subsidies directly to your monthly payment (reducing what you pay now) rather than waiting for tax time. For families living paycheck-to-paycheck, this cash flow matters.

The Bottom Line for High-Need Families

The cheapest health insurance plan isn’t the best plan for families with chronic conditions. Your real goal is minimizing total out-of-pocket costs—premiums plus deductibles plus copays—while ensuring your family’s specific medications and specialists are covered.

For 2026, that likely means a Silver plan with cost-sharing reductions if you qualify, or a Platinum plan if you’re above CSR income limits. L.A. Care and Molina offer the lowest premiums, but Kaiser’s integrated model might save you money and stress through better specialist coordination.

Start with Covered California’s calculator today. Spend 15 minutes analyzing drug formularies. Call one insurer to verify specialist access. These small steps prevent thousands in unexpected medical debt.

Your family’s health shouldn’t require choosing between affording premiums and affording care. The 2026 marketplace has options that cover both—you just need to know where to look.

Unlock Full Article

Watch a quick video to get instant access.