Unlock 4% Rates in a 6% World: The Insider Secrets to Rate Buydowns, Points, and Builder Tricks Crushing Your 2026 Mortgage Payments

Frustrated by Stubborn 6%+ Rates? Smart Buyers Are Slashing Payments Without Waiting for a Miracle Drop

Imagine locking in a 4% effective rate on your dream home purchase right now, even as headline rates hover around 6-7% in early 2026. Thousands of buyers are doing just this—not by magic, but through rate buydowns, discount points, and killer builder incentives that savvy negotiators are snapping up before they’re gone. With inventory rising and builders desperate to move new builds, these tools are more aggressive than ever, saving families **$200-500/month** in the critical early years.[1][2][4]

Don’t miss out: Over 30% of new home sales in late 2025 featured buydowns, per industry reports, and experts predict even more in 2026 as rates stay elevated.[4] This guide breaks it all down with real examples, costs, breakeven math, and step-by-step moves to get your rate down today. Act fast—these concessions vanish when markets shift.

What’s a Rate Buydown? The Game-Changer You’re Overlooking

A rate buydown is prepaid interest (via cash or seller contribution) that temporarily or permanently drops your mortgage rate. In today’s ~6% environment, it’s the #1 tactic top agents recommend for buyers who can’t (or won’t) wait years for rates to fall.[2][5]

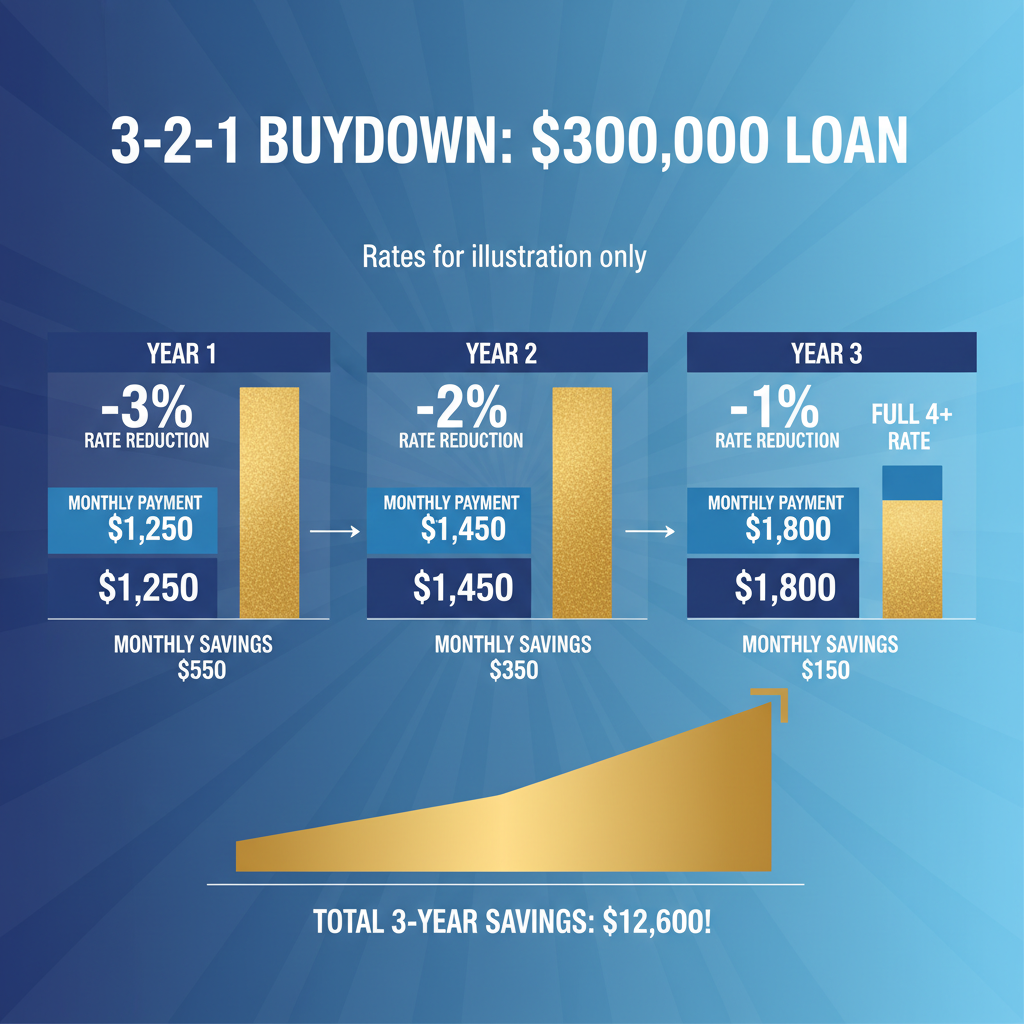

Temporary Buydowns (most popular): Builders or sellers fund an escrow account to subsidize your early payments. The gold standard is the 3-2-1 buydown: If your note rate is 7%, you pay 4% Year 1, 5% Year 2, 6% Year 3, then full 7%.[1][2] Real example from Rocket Mortgage: On a $300K loan at 7%, payments drop from $1,996/mo to $1,432 (Year 1 savings: $564/mo!).[1]

- 2-1 Buydown: 2% off Year 1, 1% off Year 2. Costs ~2-3% of loan amount; perfect for short-term relief.[4]

- Builder Example: New American Funding notes builders like Lennar and D.R. Horton offering free 2-1s on select 2026 communities—saving $300+/mo initially.[4]

Permanent Buydowns via discount points: Pay 1 point (1% of loan) to drop rate ~0.25-0.375% forever.[3][5] On a $400K loan at 6.25%, one point ($4K) gets you to 6% ($2,463 to $2,398/mo; breakeven ~5 years).[5]

Hot 2026 Products Crushing Rates

Rent to Retirement’s 5%-Down New Build Loan: Locks rates as low as 3.99% on rentals or primaries with builder concessions. Pair with their price reduction or cash-back options—ideal for investors.[3]

Rocket Mortgage 3-2-1: Custom buydowns on conventional loans; recent clients report effective 4-5% starts on 7% notes.[1]

Amerisave’s guide highlights lender-funded 2-1s for high-rate environments, with ARMs as backups (3/1 ARM starts 1-2% below fixed).[2]

Builder Incentives: Free Money Hiding in Plain Sight

Builders are in panic mode—2025 saw a 25% surge in incentives as sales slowed.[4] In 2026, expect Lennar’s ‘Rate Lockdown’ (3-2-1 buydowns on 90% of inventory) and D.R. Horton’s Total Price Reduction (use savings for points).[3][4] Social proof: ‘Buyers closing last month saved $15K+ upfront,’ says New American Funding’s Margaret Heidenry.[4]

Trend Alert: 40% of new builds now include buydowns, up from 10% in 2024, per economist forecasts. With rates ‘stuck in low-6s,’ refinancing in 3-5 years makes temporary deals a no-brainer.[2][5]

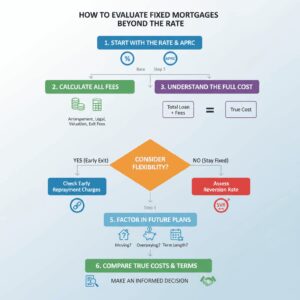

Step-by-Step: How to Score Your Buydown Deal Today

- Get Pre-Approved with Buydown Options: Hit Rocket Mortgage or Amerisave for a rate sheet showing point pricing. Ask: ‘What’s my 3-2-1 cost?'[1][2]

- Target New Builds: Search Lennar/D.R. Horton sites for ‘incentive’ listings. Example: $450K home with free 2-1 = $400/mo savings Year 1.

- Negotiate Seller Concessions: In buyer’s markets (most metros late-2025), demand 3% toward buydowns. Script: ‘Cover my 2-1, or drop price $10K.'[3]

- Run Breakeven Math: Formula: Cost of points ÷ monthly savings = months to recoup. Ex: $12K for 1% drop on $300K loan ($197/mo save) = ~61 months. Refi sooner? Go temporary.[1][5]

- Lock with Experts: Use Lendfriend Mortgage for permanent point analysis—they project falling rates make shortsighted buys risky.[5]

Pros & Cons: Temporary vs. Permanent

| Type | Pros | Cons | Best For |

|---|---|---|---|

| Temporary (3-2-1) | Big early savings ($500+/mo), often free via builder | Rate jumps later; assumes refi | New builds, short-term owners[2][4] |

| Permanent (Points) | Forever lower payments, predictable | Upfront cash ($4K+ per point), long breakeven | Long-haul homeowners[1][5] |

Expert tip from Realtor.com: ‘Always have an exit—move or refi in 3 years.'[6]

Real Math: $400K Loan Showdown at 6.25% Base Rate

No Buydown: $2,463/mo P&I.

2-1 Buydown: Year 1 $1,960 (4.25%), Year 2 $2,212 (5.25%)—builder pays ~$8K.[4][5]

1 Point Permanent: 6% rate, $2,398/mo ($65 save; $4K cost).[5]

Total 5-Year Savings: Up to $15K with temporary + refi.

Warnings from the Pros: Don’t Get Burned

Falling rates (low-6s now, more cuts expected) favor temporary—permanent points shine if rates stall.[5] Authority alert: Cassandra Halls (2026 YouTube forecast) predicts ‘buydowns peak mid-year.'[7] Scarcity: Builder deals dry up in hot markets.

Your Move: Claim Your Lower Rate Before It’s Gone

Urgency: With 2026 rates flatlining, contact 3 lenders today for buydown quotes. Visit Rent to Retirement for 3.99% specials, or ping your agent for builder lists. Thousands are pocketing massive savings—join them now and turn 6% headlines into your 4% reality. Pre-approve today and negotiate like a pro!

Unlock Full Article

Watch a quick video to get instant access.