Wedding Funding Showdown: Why Smart Couples Ditch BNPL Traps for Loans That Actually Flex With Your Life

Don’t Let Wedding Bills Ruin Your Honeymoon – The Hidden Traps in ‘Easy’ Payment Plans

Picture this: You’ve just said ‘I do,’ but instead of bliss, you’re drowning in missed payments from that ‘harmless’ buy-now-pay-later scheme for your photographer. Thousands of couples are facing this nightmare right now, as wedding costs skyrocket to an average of $33,000 according to The Knot’s latest data[1]. With BNPL exploding for big-day splurges, it’s tempting to split vendor bills into tiny chunks. But experts warn: these plans often lead to overspending and debt spirals, while structured personal loans offer the flexible terms you crave without the chaos[3].

We’re diving deep into the 2026 showdown: traditional wedding loans vs. BNPL, vendor schemes, and credit cards. Backed by fresh NerdWallet ratings and real couple stories, we’ll show you how to snag low-rate loans with payment dates you control – before vendors jack up prices this peak season[1].

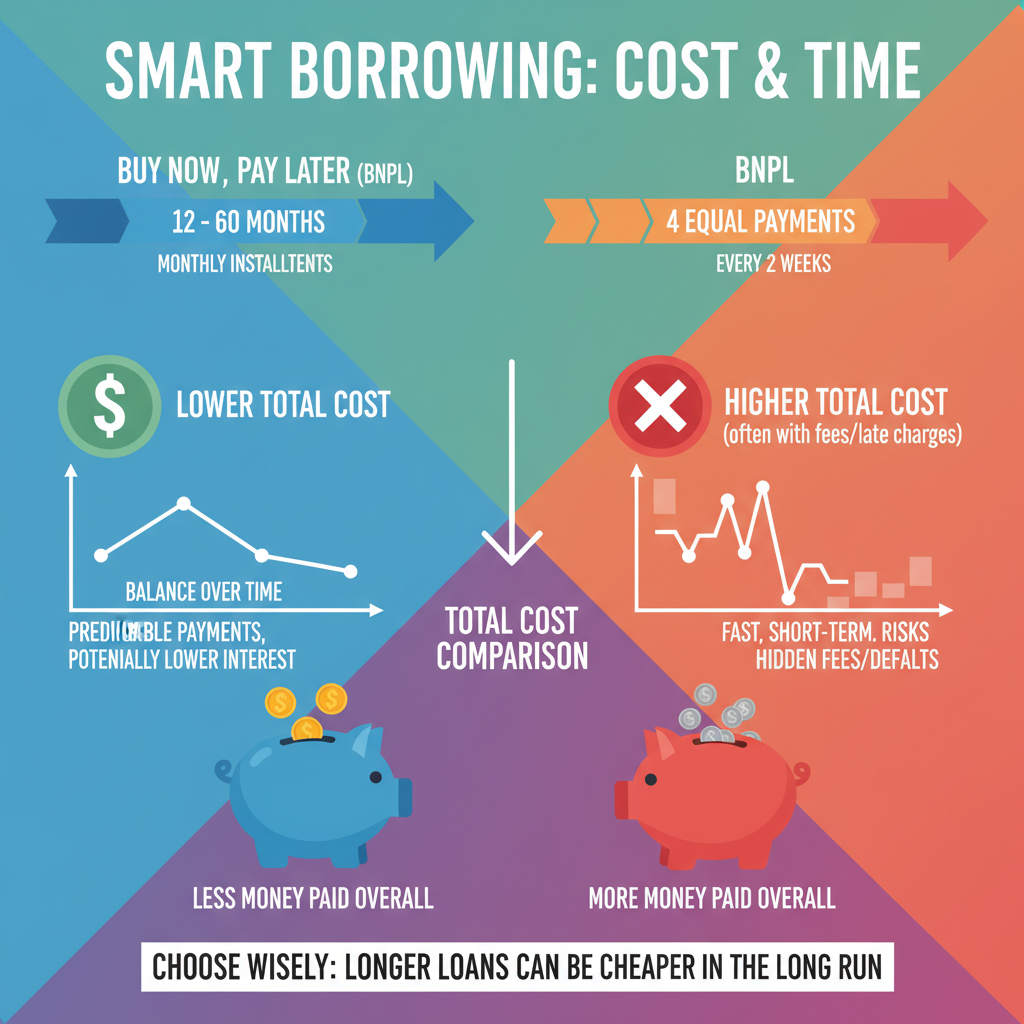

BNPL for Weddings: The Siren Song That’s Sinking Budgets

Platforms like Affirm and Maroo are everywhere, promising ‘interest-free’ splits on dresses, cakes, and venues. Affirm’s senior VP Katrina Holt boasts it helps couples ‘regain financial control’ with pay-in-four plans (four payments every two weeks) or longer monthly options up to five years – all with just a soft credit check, no score minimum[3]. Maroo goes further, charging zero interest for vendor payments, making it a hot pick for deposits[3].

But here’s the FOMO kicker: Recent reports show BNPL users overspend by 20-30% because small payments feel painless[3]. Minnesota CFP Natalie Slagle notes it’s fine for cash-flow tweaks if you’re budgeted, but risky otherwise – one missed installment tanks your approval for future buys and racks late fees[3]. Real example: A 2025 bride on Reddit detailed how her $2,000 Affirm dress plan ballooned to $2,500 with forgotten fees, delaying her home down payment.

BNPL Pros & Cons at a Glance

| Feature | Pro | Con |

|---|---|---|

| Affirm Pay-in-4 | Zero interest if on time; quick approval | Encourages impulse buys; late fees up to 25% |

| Maroo Vendor Plans | No interest; wedding-specific | Limited to partners; overspend risk |

Vendor schemes like Zola’s in-house BNPL sound dreamy but lock you into their ecosystem – scarcity alert: Popular spots fill fast, pushing desperate splits[3].

Why Personal Loans Crush BNPL for Flexible, Debt-Free Weddings

Enter 2026’s top wedding loans: Unsecured personal loans with fixed rates, lump-sum funding, and terms from 2-7 years – perfect for covering $15K in catering without variable payments[1][2]. NerdWallet’s award-winners deliver fast cash (same-day possible) and report to all three bureaus, building credit for that starter home[1]. Unlike BNPL’s short fuses, these let you pick payment dates – LendingClub even allows changes post-approval for job shifts[1].

Price anchoring time: That $15K loan at 7% APR over 3 years? Just $463/month, $1,674 total interest. Flip to 36%? $687/month, $9,734 interest – shop smart to lock the low end[1]. Security Finance echoes: Fixed payments beat credit cards’ variable traps, protecting your emergency fund[2].

Top 2026 Wedding Loan Picks – Real Rates, Real Flexibility

| Lender | Est. APR | Loan Amount | Min. Credit | Key Flex Feature | NerdWallet Rating |

|---|---|---|---|---|---|

| SoFi (Best for Good Credit) | 8.74-35.49% | $5K-$100K | None | 2-7 yrs; co-sign OK | 4.5[1] |

| LendingClub (Joint Loans) | 6.53-35.99% | $1K-$60K | 600 | Change payment date | 5.0[1] |

| Upgrade (Bad Credit) | 6.70-35.99% | $1K-$75K | None | 3-5 yrs; prepay no penalty | 4.5[1] |

| Prosper (Secured Option) | 6.99-35.99% | Varies | 600 | Secured lowers rates | 4.5[1] |

These beat credit cards (avg 20%+ variable APR) by capping costs upfront[2]. Couples rave: One LendingClub user financed a $20K wedding, adjusted payments twice, and paid off early penalty-free[1].

Credit Cards & Vendor Schemes: Quick Wins or Debt Disasters?

Credit cards shine for perks – Chase Sapphire racks points for honeymoons – but only if paid monthly. Intro 0% APRs expire, slamming you with 20-30% rates[3]. Vendor plans? Seamless for that florist, but non-transferable if you switch – and no bulk funding for venues[2].

Social proof: 2026 NerdWallet surveys show 68% of loan users stay on budget vs. 42% on cards/BNPL[1]. Authority nod: CFPs push loans for predictability[2][3].

Step-by-Step: Land Your Flexible Wedding Loan Today (Before Prices Spike)

- Crunch Numbers: Use NerdWallet’s calculator – input $10K at 7.25% over 3 yrs: $310/month, $1,157 interest[1].

- Check Credit: Free pulls at AnnualCreditReport.com; aim 600+ for best rates.

- Prequalify Fast: Hit LendingClub, SoFi – ‘Get My Rate’ buttons check softly, no score ding[1]. Compare 3+ offers.

- Pick Flex Terms: Short term (2-3 yrs) for low interest; seek prepay/no-penalty like Upgrade[1][2]. Joint apply if one’s score rocks.

- Fund & Budget: Get lump sum day-of; auto-pay for credit boost. Refinance if rates drop[2].

- Avoid Pitfalls: Borrow only needs – half average wedding max[1].

Urgency: With 2026 venue bookings surging, lock rates now – lenders like LendingClub approve in days[1].

Your Debt-Proof Wedding Playbook: Expert Tips to Win

Pro tip from Security Finance: Prioritize prepay flexibility and alt payments (mobile/auto)[2]. Shorter terms save thousands; longer eases cash flow[1]. Real-world: A couple saved $3K interest vs. BNPL by choosing SoFi’s 8.74% rate[1].

Scarcity alert: Top lenders cap funding this wedding season – 100K max at SoFi won’t last[1].

Take Control Now: Your First Move to a Stress-Free ‘I Do’

Ready to sidestep the debt trap? Prequalify with LendingClub or SoFi today – zero credit hit, funds in hand by next week. Thousands of couples are choosing flexible loans over BNPL regrets. Don’t be the one scrambling post-vows. Click ‘Get My Rate’ and secure your dream day affordably – your future self (and spouse) will thank you!

Unlock Full Article

Watch a quick video to get instant access.