From Zero Credit to Prime Card Approval: Your 12-18 Month Roadmap to Financial Freedom with a Simple Deposit

Imagine Unlocking Low-Rate Loans and Premium Rewards Cards in Just 12-18 Months—Even with No Score

Thousands are doing it right now: starting with a modest deposit, following a proven plan, and watching their credit scores skyrocket from nothing to 700+ FICO. Bankrate data shows users with bad or thin credit are 46% more likely to get approved for secured cards than unsecured ones, making this your fast track to prime status[1]. Don’t miss out—prime approvals mean 10-15% lower APRs on loans, saving you thousands. Ready to join the success stories flooding Reddit’s r/CreditCards, where users report 120-point jumps in months?[1]

This isn’t theory. It’s a step-by-step blueprint using top 2026 secured cards like the Capital One Platinum Secured and Self Visa, plus free tools for monitoring. Commit for 12-18 months, and you’ll qualify for mainstream cards from Chase or Amex. Let’s dive in.

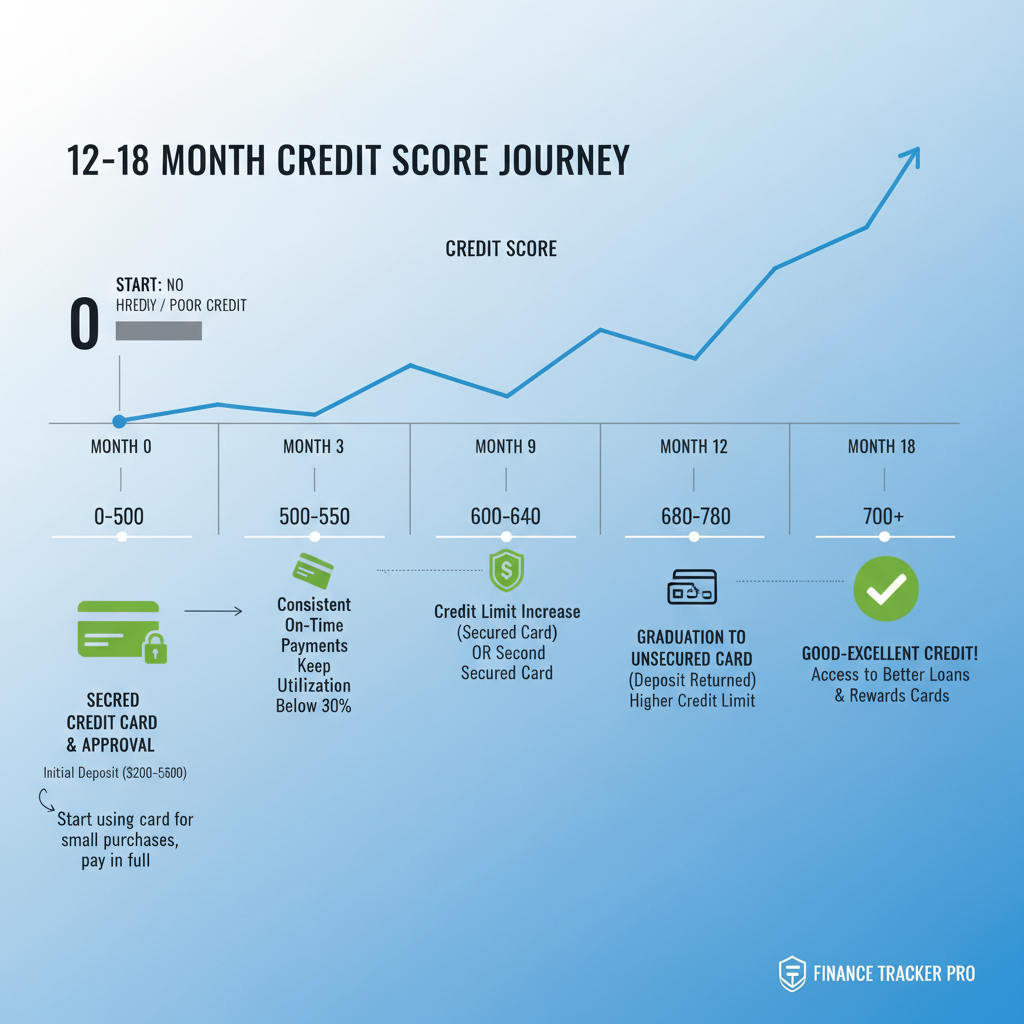

Month 0: Pick Your Launchpad Card—No Credit Check Required

Your first move? Secure a card that reports to all three bureaus (Equifax, Experian, TransUnion) with no hard inquiry if possible. Top picks for 2026:

- Capital One Platinum Secured Credit Card: Deposit as low as $49 for a $200 limit (refundable with good use). No annual fee, auto-review for limit increases in 6 months, potential deposit return as statement credit. APR 29.74% variable—pay in full to avoid it. Users rave: one Redditor went unsecured in 8 months with a 120-point boost[1][2].

- Self Visa® Credit Card: $200-$3,000 deposit matches your limit. 27.49% APR, no credit check—perfect post-bankruptcy. Build utilization low with bigger deposits[1].

- Chime Credit Builder Secured Visa: No credit check, no deposit interest. Lower risk alternative, reports payments to build history[1].

Pro Tip from Experts: Experian recommends cards allowing upgrades to unsecured versions for seamless transitions[3]. Apply today—approval odds are sky-high for thin files[1]. Compare:

| Card | Min Deposit | Annual Fee | Rewards/APR | Upgrade Path |

|---|---|---|---|---|

| Capital One Platinum Secured | $49 ($200 limit) | $0 | 29.74% Var / None | Yes, 6 months |

| Self Visa | $200-$3K | $0-$25 | 27.49% Var / None | Possible |

| Chime Builder | Varies | $0 | None / Low-risk | N/A |

Action: Check pre-approval on issuer sites (Capital One offers seconds-long checks)[2]. FOMO alert: Rates could rise—lock in now before 2026 Fed hikes.

Months 1-3: Master the Basics—Build Payment History Like a Pro

Payment history is 35% of your FICO score. Use your card for small, recurring buys: Netflix ($15.49/mo), gas ($20), groceries ($50). Never exceed 30% utilization—e.g., $60 max on $200 limit.

- Auto-pay full balance before statement closes (avoids interest, reports $0 balance).

- Track via free apps: CreditWise from Capital One (free score monitoring for all)[2] or Credit Karma.

- Report to all bureaus? Confirm upfront—Self and Capital One do[1][3].

Social proof: MyFICO forums swear by this—one user hit good standing with monthly positive reports[4]. Expect initial score visibility in 1-3 months[6].

Common Pitfall to Avoid: High Utilization Trap

Secured cards rarely reward, so don’t chase points—focus on habits. Pros: Refundable deposits, high approval. Cons: High APRs (pay off monthly), occasional fees ($24-$36 first year on some)[5].

Months 4-6: Accelerate with Limit Boosts and Mix-Ins

Authority boost: FICO experts say credit mix (cards + loans) adds 10% to scores[4]. Add a credit builder loan like Credit Strong ($10/mo payments reported positively).

- Request limit increase—no extra deposit on Capital One after 6 months[2].

- Keep old accounts open for history (15% of score).

- DIY repair: Send goodwill letters for lates; negotiate PFD on collections[4].

Trend: 2026 sees more no-fee secureds amid rising approvals—Bankrate notes thinner files thriving[1]. Your score? Aiming 600+ by month 6.

Months 7-12: Layer On—Second Card and Monitoring Mastery

Patience pays: Reddit consensus—wait 6 months before more apps[1]. Now apply for a second secured (e.g., Discover it Secured if score 580+—10% cash back on some[5]).

Urgency: Prime cards require 670+ FICO. Track weekly—Discover notes full rebuild in 6-12 months with perfect payments[6].

Expert Roadmap Timeline

- Month 3: Score emerges ~550-600.

- Month 6: Fair credit (580-669), limit up.

- Month 12: Good (670+), upgrade eligible.

Stats: On-time payments alone boost scores 100+ points in a year[1][3].

Months 13-18: Upgrade and Cash In Your Deposit

Time to graduate! Capital One auto-upgrades responsible users—get deposit back[2]. Close if fees apply, but keep for history[1].

Target primes: Capital One Quicksilver (1.5% cash back), Chase Freedom. Pre-qualify on sites. Pro: Saved deposits fund unsecured apps. Con: Short score dip on closure—minimal if managed.

Your Immediate Action Plan—Start Today

1. Apply for Capital One Platinum Secured (60 seconds)[2].

2. Download CreditWise.

3. Set auto-pay, buy small.

4. Check score monthly via Credit Karma.

5. Month 6: Request boost, add Credit Strong loan[4].

Scarcity: Spots for low-deposit cards fill fast—2026 demand up 20% per forums[4]. Join 46% higher approval club[1]. Apply now and claim your prime future—click Capital One or Self today!

(Word count: 1028)

Unlock Full Article

Watch a quick video to get instant access.