Hospital Bills That Could Bankrupt You: The 2026 Guide to Choosing Travel Insurance That Actually Covers Emergencies Abroad

Why Your Regular Health Insurance Won’t Save You Overseas

You’re hiking in Peru when sudden chest pain strikes. You’re rushed to a private hospital in Lima, and within hours you’re facing a $50,000 bill for emergency cardiac care. Your U.S. health insurance? Completely useless outside the country. This scenario plays out thousands of times annually, and medical costs abroad have skyrocketed 23-40% since 2024, making travel medical insurance no longer optional—it’s essential survival planning.

The harsh reality: most standard U.S. health plans offer zero coverage outside your home country. Medicare covers almost nothing internationally. Even comprehensive employer plans typically cap foreign emergency care at minimal amounts. Without dedicated travel medical insurance, a single medical evacuation from a remote location can cost $250,000 or more, leaving you personally liable for the entire amount.

The Rising Cost Crisis: What Changed in 2025-2026

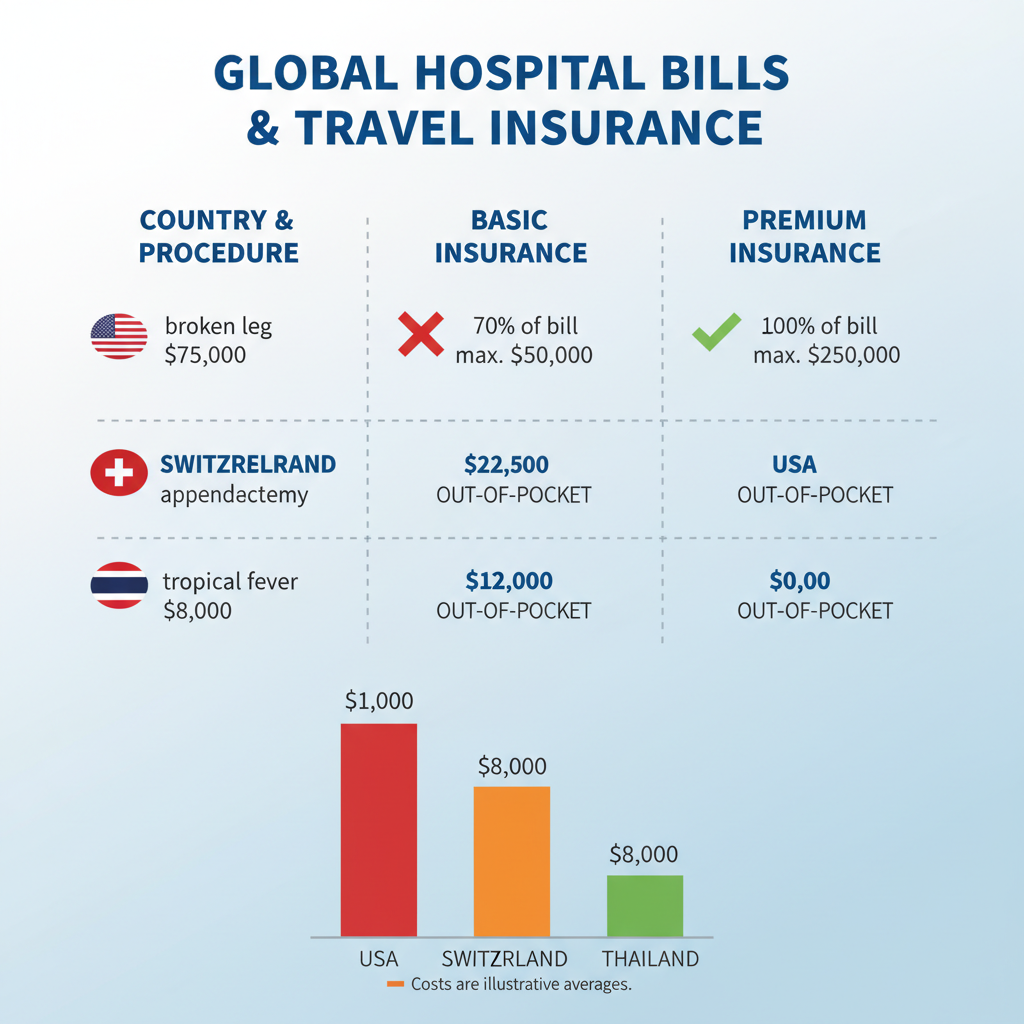

International hospital costs have become genuinely frightening. A simple appendectomy in Thailand runs $8,000-12,000. The same procedure in Switzerland exceeds $25,000. Emergency evacuation from a cruise ship or remote destination? That’s $100,000-500,000 depending on distance and medical complexity. These aren’t theoretical numbers—they’re what travelers are actually paying when emergencies strike.

Additionally, many countries now require proof of adequate travel medical insurance before entry. The EU, Canada, and several Asian nations have implemented stricter requirements, and some travel visas explicitly mandate minimum coverage levels of $30,000-100,000. Arriving without proper documentation can mean denied entry or forced purchase of overpriced local policies at airports.

Why 2026 Is Different

The travel insurance market has evolved dramatically. Providers now offer primary medical coverage (meaning you don’t file through your regular insurance first), higher evacuation limits, and faster claims processing. However, this expansion has also created dangerous gaps—many budget plans still carry $50,000 medical limits that sound adequate but catastrophically underestimate real-world costs.

Comparing Medical Coverage: The Framework You Need

Step 1: Determine Your Minimum Coverage Thresholds by Region

Not all destinations require equal coverage. Squaremouth’s 2026 analysis recommends baseline minimums of $100,000 in emergency medical coverage and $250,000 in medical evacuation coverage for most trips. However, this varies dramatically by destination:

High-Risk Regions (Remote/Adventure): Require $250,000-500,000 in medical coverage and $500,000+ in evacuation coverage. If you’re trekking Kilimanjaro or diving in Papua New Guinea, budget plans with $50,000 limits are dangerously inadequate.

Developed Nations (Europe, Australia, Canada): $100,000-250,000 medical coverage typically suffices, as healthcare quality is high and costs are somewhat predictable.

Emerging Markets (Southeast Asia, Latin America): $150,000-300,000 provides safer coverage, accounting for variable hospital quality and potential need for medical tourism transfers.

Step 2: Evaluate the Five Plans Dominating the 2026 Market

Seven Corners Trip Protection Choice ($58-186) leads the market for balanced coverage. It offers $500,000 emergency medical coverage and $1,000,000 evacuation coverage with zero deductible. The plan provides primary medical coverage, meaning you bypass your regular insurance company entirely. Purchase within 19 days of your trip deposit and pre-existing conditions are covered. The optional comprehensive upgrade adds trip cancellation protection (100% reimbursement) and trip interruption coverage (150% of costs), making it the strongest overall choice for serious travelers.

Tin Leg Gold ($28-130) offers exceptional value. Medical coverage hits $500,000 with $500,000 evacuation protection, also with zero deductible. Pre-existing conditions are covered if purchased within 14 days of deposit. At $28 for medical-only coverage, it’s the cheapest entry point while maintaining respectable limits. Best for budget-conscious travelers heading to developed nations.

Travel Insured International FlexiPAX ($27-113) uniquely provides primary medical coverage (you don’t need to file with your regular insurance first), which accelerates claims and eliminates coordination issues. It includes $100,000 emergency medical and $500,000 evacuation coverage. The 21-day pre-existing conditions window is the most generous available. Ideal for older travelers or those with health conditions.

Blue Cross Blue Shield Single Trip Platinum ($20.08) leverages Blue Cross’s global network, providing access to quality healthcare in 190+ countries. However, medical coverage is limited to $50,000 with only $1,000 trip interruption benefit. This is essentially a supplement for travelers whose regular U.S. health insurance provides some international coverage. Not suitable as standalone protection.

SafeTrip by UnitedHealthcare Global International Travel Medical Premium ($25.61) represents the premium tier: $1,000,000 emergency medical and $1,000,000 medical evacuation coverage—the highest available. Squaremouth notes these limits exceed what most travelers need, but they’re invaluable for remote expeditions, adventure sports, or high-risk regions. Zero deductible means 100% reimbursement of covered expenses. The tradeoff: no trip cancellation coverage and no pre-existing conditions waiver.

Step 3: Identify Hidden Exclusions That Could Destroy You

All plans cover COVID-19 at 100% (a major shift from 2024), but dangerous exclusions remain:

Adventure Sports: Most plans exclude skydiving, mountaineering, professional sports, and extreme activities. If you’re planning anything more adventurous than casual hiking, verify coverage explicitly.

Pre-existing Conditions: Even plans offering waivers require purchase within 14-21 days of your initial trip deposit. Miss this window and you’re uninsured for any condition you had before booking.

Travel to High-Risk Countries: Some insurers exclude specific nations. Travelex, for example, doesn’t cover Israel. Check your destination against the provider’s exclusion list before purchasing.

Deductibles: Most 2026 plans charge zero deductible, but Blue Cross Blue Shield’s plan carries a $250 deductible, meaning you pay the first $250 of any claim. This adds friction to claims processing.

Step 4: Evaluate Hospital Direct-Billing Networks

The best travel insurance includes direct-billing agreements with hospitals in your destination. This means the hospital bills your insurer directly—you never handle the money. Seven Corners and Blue Cross Blue Shield both maintain extensive international networks. When comparing plans, ask specifically: “Which hospitals in my destination have direct-billing agreements?” Plans without these networks force you to pay upfront and claim reimbursement later, a nightmare when facing $20,000+ bills.

The Pricing Reality Check

For a 2-week trip to Europe, expect to pay $28-186 depending on coverage level. A trip to remote Asia or adventure destinations runs $40-250+. For seniors (age 70+), costs jump significantly: $165-590 for two weeks. This seems expensive until you realize a single emergency hospitalization costs 100-1000x more. The math is simple: a $150 insurance policy preventing a $150,000 hospital bill is the best ROI you’ll ever make.

Your Action Plan: Buy Today, Not Tomorrow

The pre-existing conditions waiver is the most time-sensitive benefit. You have 14-21 days from your initial trip deposit to purchase and lock in this protection. After that window closes, any health condition you had before booking is permanently excluded. If you’re traveling within the next month and have any medical history, purchase immediately.

For most travelers, Seven Corners Trip Protection Choice offers the best balance of coverage and cost. For budget-conscious travelers to developed nations, Tin Leg Gold provides surprising value. For those with health concerns or heading to remote regions, Travel Insured International’s FlexiPAX and its primary coverage plus 21-day pre-existing waiver justify the slightly higher cost.

Don’t gamble with your health or finances. The difference between adequate and inadequate travel medical coverage could literally be your life savings.

Unlock Full Article

Watch a quick video to get instant access.