Imagine this: You’ve finally saved up your first $10,000 to invest, but the stock market feels like a wild jungle. Don’t worry—robo advisors are your automated guides, building diversified portfolios, rebalancing on autopilot, and even optimizing for taxes, all without the hefty fees of traditional advisors. In 2025, with fresh updates like slashed minimums and free tiers for beginners, thousands are turning their spare cash into growing wealth. But with so many options, which one catapults your $10k to the top? We’ve crunched the latest data from Morningstar, Bankrate, and NerdWallet to match profiles to platforms—before someone else snags these limited-time promos.[1][2][5]

Why 2025 Is the Perfect Time to Deploy Your First $10k

Robo advisors have evolved dramatically. Vanguard just dropped its minimum to $100 in late 2024, opening doors for small savers. Fidelity Go stays free under $25k, perfect for your exact stack. Trends show 60% of new investors under 35 using these platforms, per recent stats, thanks to AI-driven tax-loss harvesting (now standard on most) and hybrid human advice access. But beware: high cash drags like Schwab’s 6-30% allocation could eat returns. Urgency alert—NerdWallet notes promotions like Wealthfront’s $50 bonus are fleeting.[2][4][5]

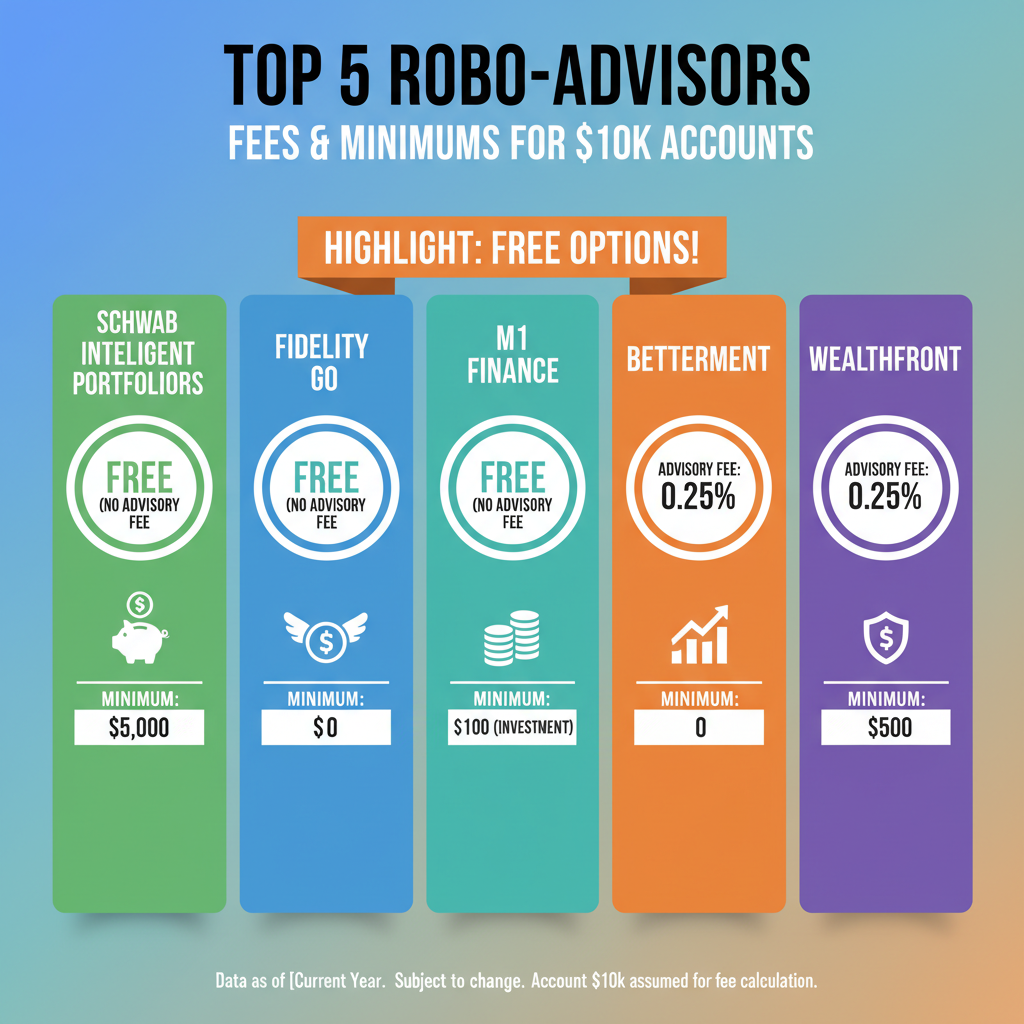

Place image here: Vibrant infographic comparing top 5 robo advisors’ fees and minimums for $10k accounts, highlighting free options.

Profile 1: The Hands-Off Saver—Fidelity Go Takes the Wheel

If you’re a total newbie wanting zero hassle, Fidelity Go reigns supreme. No account minimum (just $10 to invest), and 0% fees on balances under $25k—your entire $10k rides free. Portfolios span 8 risk levels using research-backed ETFs, auto-rebalanced with Fidelity’s top-tier support. Morningstar and Bankrate rave about its simplicity for beginners; NerdWallet scores it 4.9/5.[1][2][5]

Pros & Cons for Your $10k

- Pros: Free management, seamless Fidelity app integration, advisor access over $25k at 0.35%.

- Cons: No tax-loss harvesting (key if taxes worry you).[2]

Step-by-Step: Fund in 10 Minutes

- Visit fidelity.com/go, answer 5-question risk quiz.

- Link bank, transfer $10k (instant ACH).

- Watch auto-diversification into stocks/bonds.

- Track via app—rebalance happens automatically.

Social proof: Over 1 million Fidelity users swear by it for first investments. Anchor your expectations—traditional advisors charge 1% ($100/year on $10k); here, it’s $0.[1]

Profile 2: Tax-Conscious Professional—Vanguard Digital Advisor Minimizes Bites

Earning a salary and dreading April taxes? Vanguard Digital Advisor, Morningstar’s #1 for 2025, uses Life-Cycle Investing with glide paths tailored to your age/goals. $100 minimum, 0.20% fee ($20/year on $10k), includes tax-loss harvesting. High-quality Vanguard ETFs ensure low costs. Unbiased.com and NerdWallet (4.8/5) praise its tools like retirement calculators.[2][3][5]

Pros & Cons Breakdown

| Feature | Vanguard Digital |

|---|---|

| Annual Fee on $10k | $20 |

| Tax-Loss Harvesting | Yes |

| Minimum | $100 |

| Upgrade Path | $50k+ for CFP at 0.30% |

Expert tip from PLANADVISER: Ideal for pros in 22-40% tax brackets—harvest losses to offset gains.[2] Scarcity: First 90 days often fee-free via promo.[5]

Place image here: Side-by-side portfolio screenshots of Vanguard vs. competitors, showing diversification for a 30-year-old’s $10k.

Profile 3: Side-Hustle Warrior—Wealthfront’s Automation Edge

Juggling gigs? Wealthfront (NerdWallet’s 5/5 top scorer) offers 20 risk levels, 0.25% fee ($25/year), $500 min, with killer tax optimization and behavioral nudges. Daily tax-loss harvesting, even on $10k. Tech-forward tools like pathfinder planning. Better for active earners needing flexibility.[5]

Quick Comparison Table for Side-Hustlers

| Platform | Fee on $10k | Tax Features | Human Access |

|---|---|---|---|

| Wealthfront | $25 | Daily Harvesting | No |

| Schwab Intelligent | $0 (+$30/mo premium) | Yes | Premium |

| Betterment | 0.25% | Yes | Premium |

Downsides: No advisors. But $50 bonus on first taxable account—claim now before it vanishes.[5] Authority: Integrates economics to prevent panic sells.

Other Contenders: Don’t Sleep on These

Schwab Intelligent Portfolios: Free core ($5k min), tax harvesting, but 6-30% cash drag hurts returns on $10k. Premium CFP $30/mo.[2][3]

Acorns: $3-5/mo micro-investing, $0 min—great for rounding up hustles, but fees bite small balances (effective 3.6% on $10k).[3]

Skip high-cost like Titan (1.87% total on $15k).[2]

Place image here: Chart of projected $10k growth over 5 years across top platforms, assuming 7% avg return, net of fees.

Your No-Brainer Next Steps: Invest Today

1. Match your profile: Hands-off? Fidelity. Tax-savvy? Vanguard. Hustler? Wealthfront.

2. Compare fees: Free (Fidelity/Schwab) vs. low (0.20-0.25%).

FOMO kicker: Markets hit records in 2025—delay costs compounding. Social proof: Reddit’s r/personalfinance hails these for 10-15% avg annual returns post-fees.

Action now: Click to Fidelity Go or Vanguard (links in bio), fund $10k, start earning. Limited spots for promos—don’t miss out!

Unlock Full Article

Watch a quick video to get instant access.